In 2021 the CCP LIBOR transitions were an evolving science, with many distinct dress rehearsals and transitions. As we approach the 2023 transition the processes are being subtly updated to address some of the earlier shortcomings. Here we investigate the prevailing challenges and the variations between the three largest CCPs by USD volume – LCH, CME and EUREX – to highlight the practical steps that holders of cleared USD derivatives should be taking ahead of the primary transition weekend in May 2023.

At first glance the CCP USD transition will look very similar to those in 2021. On 20th May 2023 the CCPs will early terminate existing USD LIBOR swaps and replace with equivalent RFR products. The transition will preserve the last fixing prior to cessation, and will provide a fee that compensates for the valuation difference between the old LIBOR transaction and the new RFR plus a ’preserved fixing’ package. In common with 2021 any Basis Swaps will be split to allow the transactions to be transitioned through the same process as the swaps, and, just like 2021, the CCPs will be charging maintenance and conversion fees for your LIBOR transactions to encourage you to transition ahead of the big bang in May.

In common with 2021, and as you would expect, all trade reference will change due to the termination/rebook, so if you have any processes where mappings are manually maintained, for example hedge relationships, then this will need to be managed.

These transitions are being done to you and will happen in May whether you’re ready or not, so although it all sounds very familiar the CCPs will again run test cycles and pre-transition impact reporting to arm you with all the tools you need to make this a success.

But what of the difficulties faced in 2021, and how have these been addressed?

Clearly one of the big differences is the timing. Instead of running into a year-end this transition has the year-end during the preparations. This has the impact of giving the impression of having more time than we have, and for the year-end financial close to impact member preparations. Let’s look at the now confirmed timings:

| CCP | Basis Swaps | Primary Transition | ZCS, VNS |

|---|---|---|---|

| LCH | 21/April | 19/May | 21/April |

| CME | 24/March | 21/April | 03/July |

| EUREX | tba | 21/April | tba |

And here are the Dress Rehearsals dates:

| CCP | Dress Rehearsal 1 | Dress Rehearsal 2 |

|---|---|---|

| LCH | 24/February | 31/March |

| CME | – | – |

| EUREX | 28/February – 02/March | 21/March – 23/March |

What else is different? Clearly volumes are considerably higher for USD than the combined volumes of the transitions that have gone before. In 2021 we heard of organisations that struggled to process the GBP terminations/rebookings in the window available, so this will need to be assessed.

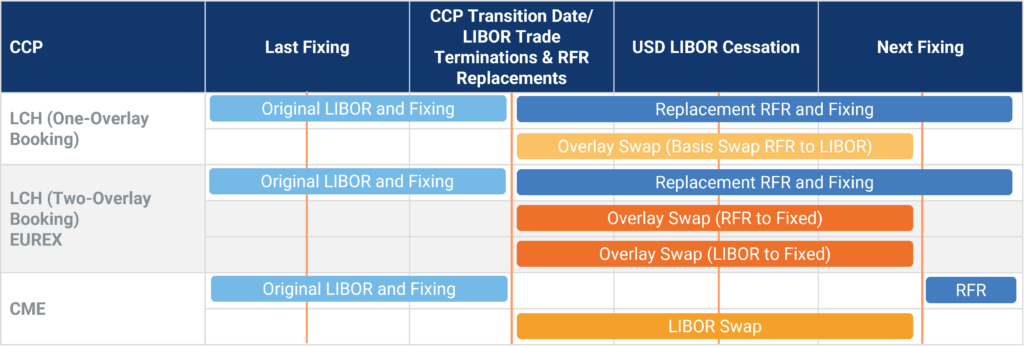

For the LCH, fees will be distributed via a stand-alone compensation swap, whereas the CME will include the compensation as a fee in the replacement RFR trade.

The LCH method of preserving the last fixing, their ‘Overlay Swap’, remains unaltered, but the revised CME proposal is to issue a forward start RFR replacement starting on the date of the first reset post cessation, and a LIBOR swap covering the period from transition to the day before first reset post cessation, so there will only be one live cashflow.

Veterans of the 2021 transition will remember that the LCH’s ‘Overlay Swap’ method leaves members with increased notionals for the period between transition and the fixing after cessation. The LCH are looking into methods to reduce this impact, but at present these seem to be limited to advice to run compressions (solo and multilateral), however, as they point out, by performing the transitions in H1 the majority of Overlay Swaps will have matured before 2023 year-end reporting where notional increases were most problematic.

As well as performing the Basis Swap split on a set date the LCH will also provide a tool to allow members to orchestrate their own Basis Swap split ahead of the universal split in April. This is a useful addition as members will be able to customise their test cycles to their own books of work. One point to note. The LCH tool will standardise the fixed leg attributes from these member-initiated splits to align with the most common market conventions. This will have the effect of allowing more compression opportunities, butopportunities but may result in slightly mismatched flows – we will understand more before the tool is released.

There are some additional considerations such as the treatment of swaps with back-end stubs where the CME will use an additional forward starting swap for the stub and replace the stub period in the RFR with a zero-coupon period. For these swaps with back-end stubs, the CME will interpolate the final stub rate whereas EUREX will provide compensation instead.

Although there are some details to iron out, members can start to plan and build the CCP transitions into their H1 2023 books of work.

It will be important to understand how you intend to manage the Basis Swap transition. The Basis Swap transition is reasonably close to the primary transition, so members should make sure they have the bandwidth to test both of these or , where the option is provided, to perform elective Basis Swap transitions as soon as it is viable to do so. A future article will further explore the difference between elective Basis Swap transitions and those at the mandatory date.

How exhaustively you test through the Dress Rehearsals will probably be driven by your experience from the 2021 transitions. You should confirm which CCPs you are clearing through, and understand the variations in their transition process, also consider whether the USD volumes will cause a processing issue. If there are concerns relating to the update of trade references, then you will be testing more extensively. The Dress Rehearsals are an opportunity to take some uncertainty out of the transition, so take some time to understand what trades you will be loading into the CCP test environments.

To cut down on the maintenance/conversion fees, and to reduce the number terminations/re-bookings (with associated overlays and compensations), perform solo and multi-lateral compressions. The closer to the transition dates the better, but the reality may well be that this is done in late 2022 to avoid year-end and to give early visibility of likely transition volumes and impacts.

Brickendon with provide a further update when CCPs release plans.

Explore the latest $IBOR insights from Brickendon and ensure that your organisation is ready for IBOR reform.